The Hidden Cost Sitting in Your Insurance Renewal

Commercial fleet insurance rates have climbed steadily across every market segment, from small local service fleets to regional trucking operations running 200 vehicles. Underwriters price risk based on what they can see: claims history, driver safety data, and a fleet's ability to document and resolve incidents quickly. Without video evidence, insurers see a black box. They price accordingly.

Dash cameras change that equation. A growing number of commercial carriers now offer measurable premium reductions to fleets that deploy connected cameras, maintain documented safety programs, and bring verifiable behavioral data to renewal conversations. The discounts exist. Qualifying for them requires deliberate preparation.

What Insurers Actually Look For

Not every fleet with cameras automatically earns lower premiums. Insurers vary widely in how they structure discount programs and what evidence they require before adjusting rates. Understanding their evaluation criteria puts fleet managers and CFOs in a much stronger position before a renewal conversation begins.

Safety Performance Data and Trend Lines

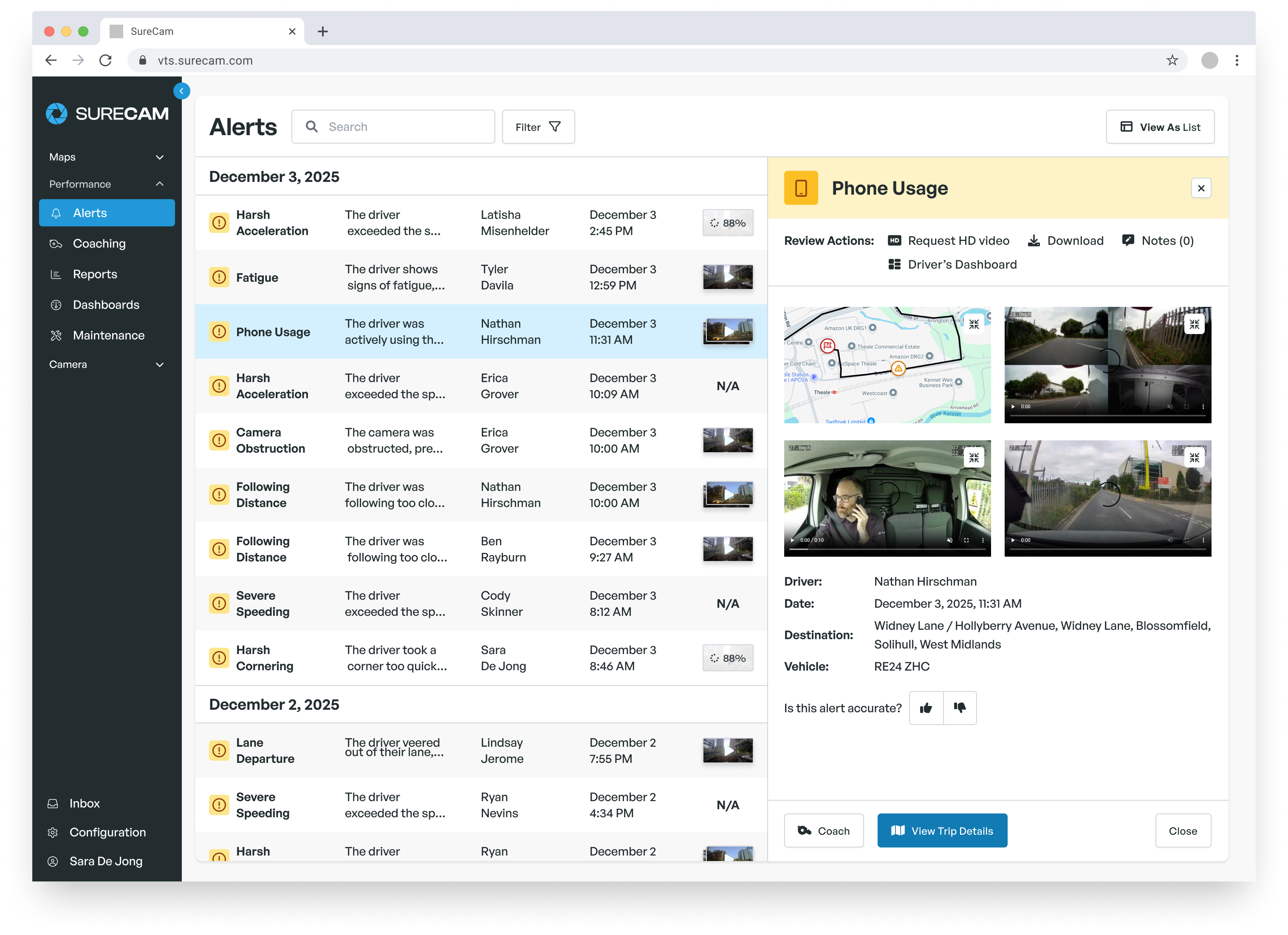

Insurers want to see that cameras changed behavior, not just recorded it. The metrics they prioritize typically include hard-braking frequency, harsh acceleration events, speeding incidents above posted limits, and collision rates over a rolling 12-month period. A downward trend across these indicators signals a safer fleet. A flat line suggests cameras went in but nothing changed.

The practical implication: begin pulling monthly safety performance reports from the moment cameras go live. Most connected dash cam platforms generate these automatically. The goal is to build a 6-to-12-month data record before a renewal conversation begins. Carriers want trend evidence, not a single snapshot, because a single snapshot tells them nothing about whether improvement holds.

Claims History and Resolution Speed

Insurance underwriters place significant weight on how quickly a fleet resolves open claims and how often those claims result in at-fault settlements. Video footage shortens this timeline in two ways. First, it allows a fleet to establish liability rapidly at First Notification of Loss (FNOL), which reduces investigative back-and-forth. Second, it defeats false and exaggerated claims before they enter lengthy litigation.

A fleet that enters renewal with zero open claims and a documented record of fast, video-supported resolutions represents a measurably lower risk than one with several contested incidents. That difference shows up directly in how underwriters categorize the account.

Documentation of a Formal Safety Program

Many carriers require more than hardware. They want evidence of a safety program: written policies, documented driver training, a coaching cadence tied to camera alerts, and records showing that management acts on unsafe events. Fleets that can produce a safety playbook alongside their telematics data tend to receive the most favorable treatment.

This requirement trips up smaller fleets most often. Cameras get installed, incidents get reviewed reactively, but the documentation never materializes. Before approaching a carrier about discount eligibility, make sure the safety program generates records that can survive a carrier audit.

How Fleet Size Shapes the Conversation

The discount structure and negotiation approach differ significantly by fleet size. The table below summarizes how the conversation typically plays out across three tiers, though specific percentages vary by carrier and state.

| Fleet Size |

Typical Discount Levers |

Negotiation Priority |

| 10 vehicles |

Program eligibility, claims history cleanup, FNOL process |

Demonstrate a formal safety program; even 1-2 at-fault incidents can dominate the rate |

| 50 vehicles |

Behavioral data trends, false claims documentation, driver scorecards |

Present 12-month improvement data; target contested claims as the biggest rate driver |

| 150+ vehicles |

Portfolio-level risk reduction, self-insured retention options, and loss development improvement |

Negotiate with the data package; the underwriter will model expected future losses |

Small Fleets (Around 10 Vehicles)

For a fleet in this range, the insurance premium per vehicle can fluctuate dramatically based on even one or two claims. A single at-fault accident in a policy year can raise rates across the entire account. The discount opportunity here has less to do with aggregate data and more to do with removing specific high-risk factors from the underwriter's view.

Installing connected cameras, building a documented safety review process, and going 12 months without a paid at-fault claim creates a clean renewal story. Imagine a 10-vehicle HVAC service fleet that previously averaged two disputed claims per year. After cameras, those disputes resolve quickly with video evidence, and the fleet enters renewal with a materially improved loss history. That kind of outcome, documented and presented clearly, gives an underwriter concrete reason to adjust the risk classification.

Mid-Sized Fleets (Around 50 Vehicles)

Fleets in this range typically generate enough behavioral data to support a statistical argument. Monthly driver scorecards, harsh event frequency trends, and false-claim documentation all become meaningful inputs to an underwriter's loss model. The conversation shifts from "cameras installed" to "here is what changed because of cameras."

Imagine a 50-vehicle concrete delivery fleet that tracks harsh braking events monthly. Over 12 months, that metric drops by more than half. Third-party claims also decline. The safety manager can present a clear data package showing the behavioral change, the claims reduction, and the faster average resolution time per incident. Underwriters reward that kind of narrative because it demonstrates that the safety investment produced outcomes, not just intentions.

Larger Fleets (150+ Vehicles)

At this scale, insurers often assign a dedicated underwriting analyst to the account. The discount opportunity extends beyond premium rate to include self-insured retention thresholds, loss development factors, and loss-sensitive program structures. A fleet with strong data loses little by pushing for a self-insured component because it has the evidence to support lower expected loss frequency.

Larger fleets should arrive at renewal with a formal data package: 12-to-24 months of behavioral trend data, a claims loss run showing at-fault frequency and dollar amounts, documentation of coaching interventions tied to camera events, and any false claims defeated with video. This transforms a renewal negotiation into a risk presentation, which generates more favorable underwriting decisions than a rate discussion alone.

What Disqualifies Fleets (and How to Avoid It)

Several common patterns cause carriers to decline discount requests or limit the benefit even when cameras sit in every vehicle.

Data that exists but never gets shared. Cameras capture events automatically, but many fleet managers never pull the reports in a format that carriers can evaluate. The solution: establish a standing monthly report cadence and store reports in a file accessible during negotiations.

Inconsistent coaching documentation. A carrier reviewing a discount request wants to see that harsh events triggered coaching conversations. If drivers receive alerts but no follow-up action appears in the record, the carrier cannot confirm that behavior changed. Document coaching sessions, even briefly, in the fleet management system.

Cameras on only part of the fleet. Partial deployment creates an asymmetric risk profile. Underwriters often treat partial coverage as a red flag: if cameras reduced risk, why did management not extend them to every vehicle? Full-fleet deployment signals commitment to the safety program as standard practice.

Poor FNOL process. Fast claims resolution requires a clear process for the first 24 hours after an incident. Fleets without an FNOL workflow miss the window where video evidence carries the most leverage. Carriers notice whether fleets resolve claims quickly or let them age.

How to Build Your Case Before Renewal

The most effective time to start preparing starts well before the renewal date, ideally 6 to 9 months out. The preparation steps follow a logical sequence.

Start by auditing what data the current platform generates and whether it exports in a carrier-readable format. Most commercial underwriters want summary-level metrics, not raw event logs. Some carriers have specific data intake formats; ask the broker whether the carrier has a preferred submission template.

Next, review the open claims file. Identify any claims where video evidence could accelerate resolution or support exoneration. Closing open claims before renewal strengthens the loss run more than almost any other single action. Every closed-with-no-payment item on the loss run improves how underwriters model future expected losses.

Then assemble the safety program documentation. Written driver policies, training records, coaching logs tied to camera events, and any formal safety certifications all belong in the package. Carriers treat this documentation as evidence that the organization manages safety as a function, not a reaction.

Lansberry Trucking, an 80-truck US carrier, saw claims losses drop 80% in a single year after deploying SureCam's network-connected cameras. Founder Sam Lansberry II framed the investment plainly: "I don't view our investment in SureCam as a cost, it's a profit-center. Last year alone, our claims losses reduced by over 80%." That kind of documented performance, presented to an underwriter with the underlying data, makes a compelling case for preferential treatment at renewal.

When to Negotiate and What to Ask For

Timing matters. Most commercial carriers lock rate adjustments at the renewal quote stage, which typically runs 60 to 90 days before expiration. Presenting data at that point, rather than reactively at expiration, gives the underwriter time to modify the risk model.

The direct questions worth asking: Does the carrier offer a formal telematics or dash cam discount program? What data format does it require? Does partial deployment qualify, or does the discount apply only at full-fleet coverage? Some carriers have structured discount schedules; others evaluate on a case-by-case basis. Knowing which situation applies before the conversation starts prevents leaving documented savings on the table.

For fleets with strong safety data and improving loss history, it also makes sense to ask about alternative program structures: captive programs, risk-sharing arrangements, or higher-deductible structures in exchange for lower base rates. Mid-sized and larger operations with clean data may find these more cost-effective than standard market pricing.

The Longer-Term Premium Strategy

Insurance discounts from dash cameras tend to compound over time. Year one often reflects carrier skepticism: the data record is short, and the discount reflects the equipment's presence more than its impact. By year two or three, a fleet with consistent behavioral improvement and a clean claims record has earned a track record that carries real actuarial weight.

The compounding effect works in both directions. A fleet that installs cameras, earns an initial discount, and then lets the safety program atrophy will see that reflected in its data. Treating video telematics as an active management tool rather than a set-and-forget system protects the premium gains the investment generated, and positions the fleet to move into lower risk tiers as the data record grows. Speak with one of our experts today, and we can help you work with your insurance broker. Book your call here today.

.png)

.png)